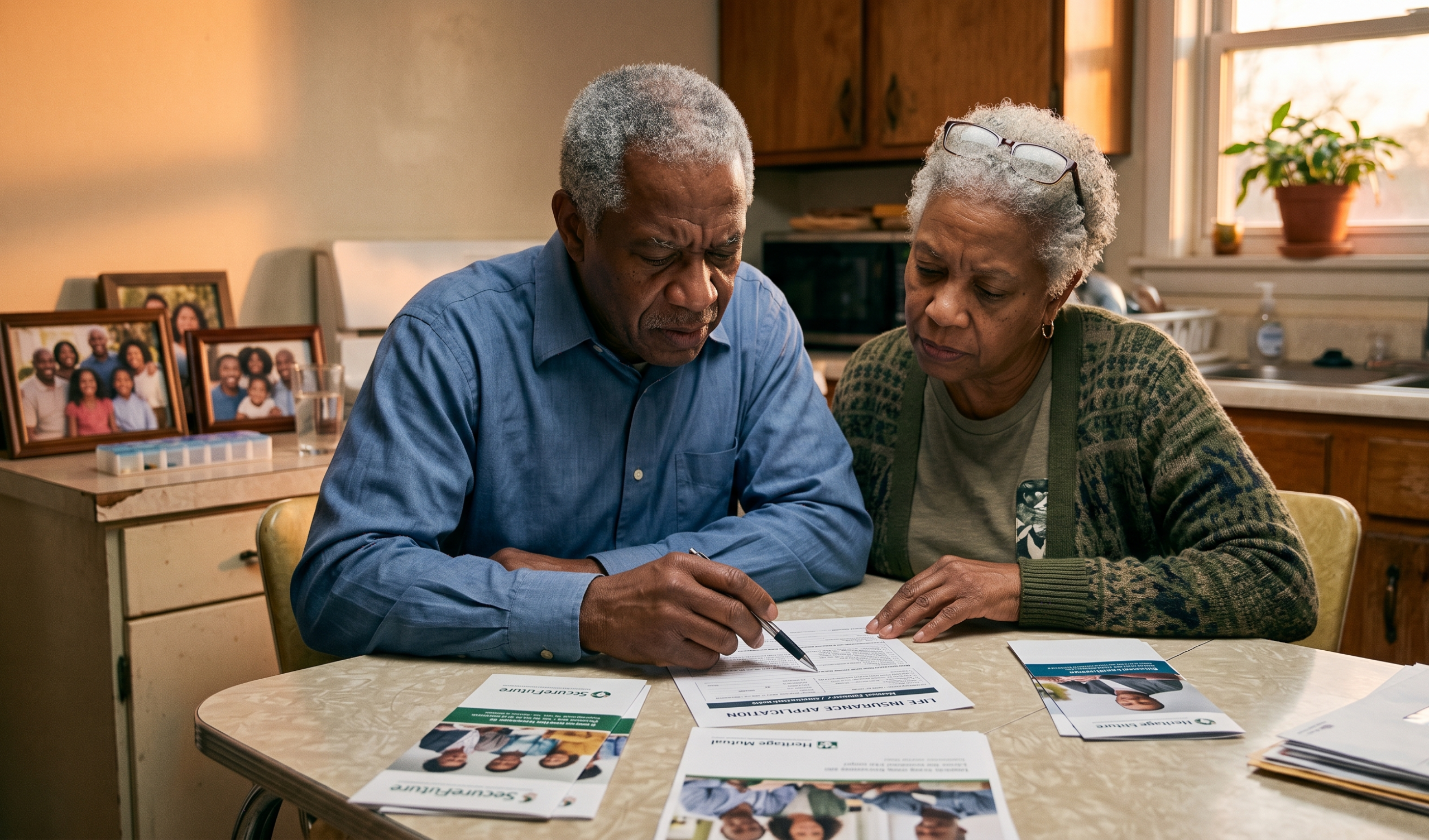

Can You Get Life Insurance With Diabetes,Heart Disease, or COPD?

If you've been turned down for life insurance before — or you've assumed a health condition putscoverage out of reach — this post is for you. A prior decline doesn't mean the door is permanentlyclosed. It usually just means that particular policy, from that particular company, wasn't the right fit.

The Myth: One ‘No’ Means No Coverage — Ever

Being declined for a traditional life insurance policy can feel final. It isn’t. Traditional policies — the kind that require full medical underwriting, blood tests, and doctor’s records — have strict health standards. Final Expense life insurance operates under a completely different set of rules. Many people who were turned

away from conventional coverage qualify for Final Expense policies without any medical exam at all.

The goal of Final Expense insurance isn’t to insure only perfectly healthy people. It’s to help seniors cover end-of-life costs: funeral expenses, burial, outstanding medical bills, or small debts they don’t want to leave behind. Insurers offering these policies understand that their customers are often managing chronic

conditions — and they’ve built products accordingly.

Why Health Conditions Matter Less for Final Expense

Traditional life insurance is designed to last 20, 30, or even 40+ years. Insurers take on significant risk over that time, so they screen carefully. Final Expense policies, by contrast, are smaller whole life policies —typically between $5,000 and $25,000 in coverage — with shorter expected benefit periods. That smaller

risk profile allows insurers to accept applicants with health histories that would disqualify them elsewhere.

Additionally, Final Expense policies are permanent. Once issued, your premium won’t increase and your coverage won’t be canceled because your health changes later. For someone managing a chronic condition, that stability matters enormously.

Guaranteed Issue vs. Simplified Issue: Explained Simply

There are two main types of Final Expense policies. Knowing the difference helps you shop smarter.

|

Feature

|

Guaranteed Issue

|

Simplified Issue

|

|---|---|---|

|

Medical questions?

|

None

|

A few yes/no questions

|

Guaranteed Issue means exactly what it sounds like: if you’re within the eligible age range (typically 50–85), you’re approved — no health questions asked. Premiums are higher because the insurer takes on unknown risk, and nearly all guaranteed issue policies include a graded benefit period for the first two years.

Simplified Issue involves answering a short set of health questions — usually 5 to 15 — but no medical exam. If your condition is being managed and you don’t have a recent hospitalization or terminal diagnosis, you may qualify for simplified issue, which typically offers lower premiums and full immediate coverage

Condition-by-Condition Breakdown

Diabetes

Diabetes is one of the most common conditions among Final Expense applicants, and it’s generally well-accommodated.

Type 1 diabetes managed with oral medication typically qualifies for simplified issue coverage. Many carriers view oral-medication management as a sign of a stable, controlled condition. Premiums may be modestly higher than a non-diabetic applicant, but coverage is usually available at

standard or mildly rated terms.

Type 2 diabetes managed with insulin is more nuanced. Some carriers offer simplified issue to insulin-dependent Type 2 diabetics; others route these applicants to guaranteed issue. Much depends on age of diagnosis, whether complications like kidney disease or neuropathy are present, and A1C levels if

asked.

Type 3 diabetes is typically covered under guaranteed issue policies. Simplified issue is possible with some carriers, but less common. If you have Type 1 diabetes with complications such as dialysis limb amputation,guaranteed issue is usually the appropriate path.

Heart Disease

A history of heart disease covers a wide range. A heart attack from 5 years ago that’s been followed with medication and lifestyle changes is a very different risk profile than a recent bypass surgery or active congestive heart failure. Generally speaking, applicants with a cardiac event more than 2 years ago — who are stable on medication — often qualify for simplified issue. More recent events, pacemakers, or active heart failure typically qualify for guaranteed issue. This is an area where shopping across multiple carriers matters significantly.

COPD

Chronic Obstructive Pulmonary Disease (COPD) is common among the 55+ population, and most carriers have built it into their underwriting. Mild to moderate COPD — where you’re managing with inhalers but not on supplemental oxygen — often qualifies for simplified issue. Severe COPD with oxygen dependency typically qualifies for guaranteed issue rather than simplified issue. The specific stage and treatment plan

matters.

Cancer History

A prior cancer diagnosis doesn’t automatically disqualify you. Many carriers look at whether you’ve been cancer-free for a specific period — commonly 2 to 5 years — after which simplified issue may be available.

Certain lower-risk cancers (such as basal cell skin cancer) are often treated more leniently. Active cancer or cancer diagnosed within the past 1–2 years typically routes applicants to guaranteed issue. A terminal diagnosis of any kind, however, generally puts standard Final Expense coverage out of reach

What the Application Actually Asks

Final Expense applications are designed to be simple. Simplified issue applications typically ask yes/no questions along these lines:

– Are you currently confined to a hospital, nursing home, or hospice?

– Have you been diagnosed with a terminal illness?

– Do you require assistance with daily living activities (bathing, dressing, eating)?

– Have you been treated for or diagnosed with certain conditions in the past 2–5 years? (Heart attack, stroke, cancer, HIV/AIDS, organ failure, etc.)

– Are you currently on dialysis?

These questions are looking for the most serious red flags. If you can answer ‘no’ to all of them — even with managed diabetes, COPD, or a past cardiac event — you may qualify for simplified issue. Guaranteed issue applications skip health questions entirely and only verify your age and identity

Typical Premium Ranges and Coverage Amounts

Premiums vary based on your age, gender, coverage amount, health classification, and the carrier. Here are general ranges to set expectations — actual quotes depend on your specific profile

|

Age Range

|

Simplified Issue ($10K coverage)

|

Guaranteed Issue ($10K coverage)

|

|---|---|---|

|

Ages 55–65

|

~$30–$70/month

|

~$60–$110/month

|

Coverage amounts across the Final Expense market typically run from $5,000 to $25,000 — designed to cover funeral costs (national averages currently run $8,000–$12,000) and related end-of-life expenses.

How Graded Benefit Periods Work

Important to understand before you buy: Most guaranteed issue policies and some simplified issue

policies for higher-risk applicants include a graded benefit period, typically lasting two years from the

policy issue date. During this window, if you pass away from natural causes, your beneficiaries typically

receive a return of premiums paid plus interest (commonly 10%) not the full face value. After the

two-year period ends, the full death benefit applies

Death due to an accident is usually covered at the full face value from day one, even during the graded

period. This structure protects insurers from applicants who purchase coverage while already seriously ill.

For most healthy-enough-to-wait applicants, it’s a reasonable tradeoff for getting covered without a medical

exam — but it’s worth asking about before you sign.

Type your paragraph here